Why Choose a Mutual Fund?

Mutual Fund: A Better Way to Earn Money

Have you ever heard someone say, “I invest in mutual funds,” and quietly wondered what it actually means? I used to feel the same. Whenever friends talked about SIPs, market returns, or investment plans, I would listen with curiosity but also a little confusion. It all sounded too complicated for an ordinary person like me.

That curiosity first led me to understand the stock-market-and-share-market-difference. I also realised, as I shared in 5 ways-to-live-a-simple-life-and-earn-money, that mindful financial habits can make wealth-building feel much simpler.

One day, instead of ignoring those conversations, I started asking questions. I spoke to friends who had been investing for years, read trusted resources, watched beginner-friendly videos, and slowly began understanding what a mutual fund really is. The more I learned, the more I realised that investing isn’t only for wealthy people or market experts.

I’m not a stock market analyst, financial advisor, or investment expert. I’m simply someone who wanted to understand money better, just like many of you. In this blog, I’m sharing everything that helped me learn mutual funds in the simplest way possible, so you can begin your own journey with confidence.

Whether you’re a homemaker, student, working professional, parent, freelancer, or someone planning for retirement, I hope this guide helps you understand mutual fund investing without fear. Let’s learn together, one simple step at a time.

What Is a Mutual Fund?

If I had to explain a mutual fund to my younger self, I wouldn’t start with complicated financial terms. I’d simply say it’s a smart way for many people to invest their money together instead of trying to pick stocks on their own. That simple thought changed everything for me.

When many people contribute small amounts into one common fund, experienced professionals manage that money by investing it in different places such as company shares, bonds, or other financial instruments. Instead of making every investment decision yourself, trained fund managers do the research and manage the portfolio according to the fund’s objective.

The best part? You don’t need lakhs of rupees to begin. Many mutual fund schemes in India allow you to start with just ₹100 or ₹500 through a Systematic Investment Plan (SIP), depending on the scheme.

Understanding Mutual Fund in the Simplest Way

Think of a mutual fund as a large community basket.

Instead of one person filling the basket alone, hundreds or even thousands of people contribute according to what they can afford. The basket is then looked after by professionals who decide where the money should be invested.

Here’s how it works:

- Many investors contribute money into one mutual fund.

- The money is pooled into a single investment fund.

- A professional fund manager invests it based on the fund’s goals.

- Investments may include company shares, government securities, bonds, or a combination of assets.

- Any gains or losses are shared among investors according to the number of units they own.

- Your investment value may go up or down because mutual funds are linked to market performance.

Example

Let’s imagine 100 people each invest ₹500 in the same mutual fund.

Together, the fund now has ₹50,000 to invest.

Instead of each person trying to buy different shares or bonds individually, the fund manager researches the market and invests the money across several assets to spread the risk.

If the investments perform well over time, the value of the mutual fund may increase, and every investor benefits based on the amount they invested. If markets fall, the value can also decrease. That’s why mutual funds should generally be viewed as long-term investments rather than a way to make quick money.

A Thought from My Heart

One thing that truly surprised me was this: I always believed investing was something people started only after becoming financially comfortable. But the more I learned, the more I realised that many people become financially stronger because they started investing consistently, even with small amounts. That shift in thinking made mutual funds feel much less intimidating and much more practical.

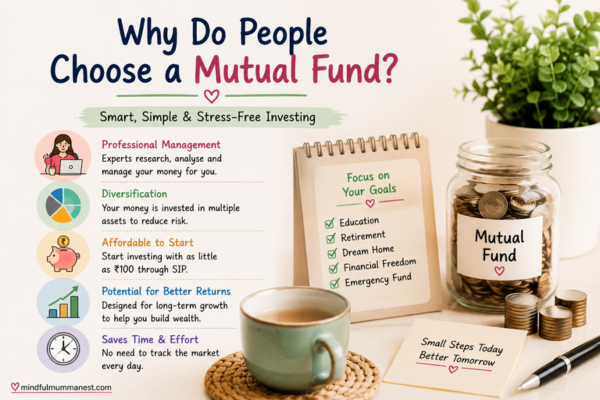

Why Do People Choose a Mutual Fund?

This was another question I kept asking myself. If people can buy shares directly, why do so many choose a mutual fund instead? The answer became clearer as I spoke with friends, explored different career and income opportunities in my guide on which-jobs-pay-the-most-in-india, and realised through my daily-routine-morning-to-night-earn-money artical that small, consistent financial habits often lead to bigger goals.

Not everyone has the time, confidence, or knowledge to study the stock market every day. Many people simply want their money to work towards future goals while they focus on their families, careers, businesses, or studies. A mutual fund offers that convenience by letting professional fund managers handle the investment decisions.

A Mutual Fund Helps You Focus on Your Goals

Every person has different dreams, but many financial goals are similar.

A mutual fund can become one way to save and invest gradually for those future needs.

People often invest in mutual funds to work towards goals like:

- Building long-term wealth.

- Creating a habit of disciplined investing.

- Saving for a child’s education.

- Planning for retirement.

- Buying a home.

- Creating an emergency financial cushion.

- Growing savings instead of leaving all the money idle in a savings account.

- Working towards long-term financial planning.

Example

Imagine Priya, a homemaker, who manages her household budget carefully.

After paying monthly expenses, she usually saves around ₹1,000. Earlier, she would keep this money aside at home because she felt it wasn’t enough to invest.

A friend suggested learning about SIPs. After understanding how mutual funds work, she decided to start with a ₹1,000 monthly SIP in a mutual fund that suited her goals.

She didn’t expect instant profits. Instead, she focused on building a healthy financial habit month after month, knowing that consistency and time can make a meaningful difference.

A Thought from My Heart

One friend shared something with me that I’ve never forgotten:

“Don’t wait until you have a lot of money to start investing. Start with what you can comfortably afford, and let consistency become your biggest strength.”

That simple advice changed the way I looked at saving and planning for the future.

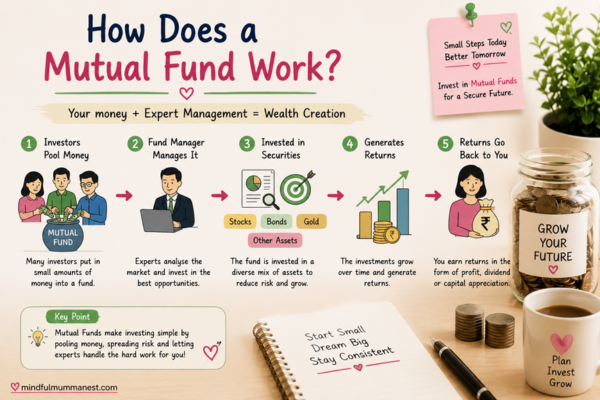

How Does a Mutual Fund Work?

When I first heard about mutual fund investing, I imagined that my money would simply sit in one account and somehow grow over time. Later, I realised that’s not how it works. Every mutual fund follows a clear investment strategy, and behind it is a team of professionals making informed decisions based on the fund’s objective.

The money invested by thousands of people is pooled together. This large amount is then invested in different assets like company shares, government securities, bonds, or a mix of these. As these investments perform in the market, the value of your mutual fund units also changes. This is why mutual funds can grow over time, but they can also experience short-term ups and downs.

How Your Mutual Fund Investment Travels

Understanding the journey of your money makes mutual funds much less confusing.

Once I understood these simple steps, everything started making sense.

Here’s how a mutual fund works:

- You invest a chosen amount in a mutual fund.

- Your money is combined with investments from many other people.

- The fund is managed by an Asset Management Company (AMC).

- A professional Fund Manager researches and selects investments based on the fund’s objective.

- The money is invested across different assets to create a diversified portfolio.

- As the market changes, the value of those investments also changes.

- Your investment value rises or falls according to the performance of the fund.

Example

Let’s say 10,000 people invest in the same mutual fund.

Some invest ₹500, some ₹5,000, while others invest ₹50,000. Together, the fund now has crores of rupees.

The fund manager doesn’t put all that money into just one company. Instead, they may invest in well-known companies, government bonds, banking stocks, IT companies, healthcare businesses, or other investments depending on the fund’s strategy.

If one sector performs poorly, other investments may help balance the overall portfolio. This diversification is one reason many beginners feel more comfortable starting with mutual funds instead of choosing individual stocks.

A Thought from My Heart

One thing I learned from talking to friends is that a mutual fund doesn’t remove market risk—it simply helps spread your investment across different opportunities. That made me understand why people say, “Don’t put all your eggs in one basket.”

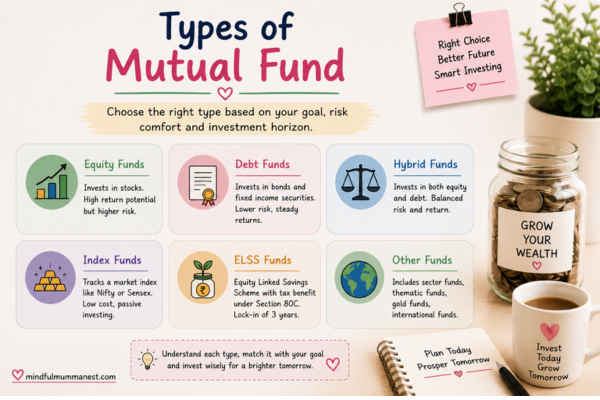

Types of Mutual Fund

When I started learning about mutual fund schemes, I was surprised to see there wasn’t just one type. Every mutual fund is created with a different purpose. Some focus on long-term wealth creation, some aim for stability, while others try to balance both growth and lower risk.

The right mutual fund isn’t the one everyone else is investing in. It’s the one that matches your financial goals, investment period, and comfort with market ups and downs.

Choose a Mutual Fund That Matches Your Goal

Just as we choose different clothes for different occasions, we should choose different mutual funds for different financial goals.

Understanding these categories makes it much easier to decide where you might begin.

1. Equity Mutual Fund

An equity mutual fund mainly invests in shares of companies. Since stock prices move up and down, these funds generally carry higher market risk but also offer the potential for higher long-term growth.

Suitable for:

- Long-term wealth creation

- Young investors

- People comfortable with market fluctuations

- Goals that are 5 years or more away

Example

A 28-year-old professional wants to build wealth over the next 20 years. Since there is plenty of time before the money is needed, an equity mutual fund may be considered after understanding its risks and suitability.

2. Debt Mutual Fund

A debt mutual fund invests mainly in government securities, treasury bills, and corporate bonds instead of company shares.

These funds are generally chosen by people looking for relatively stable returns with lower market volatility than equity funds, though they still carry risks.

Suitable for:

- Conservative investors

- Short to medium-term goals

- People who prefer lower market fluctuations

Example

A family wants to keep aside money for a vacation planned next year. Instead of taking high market risk, they may consider a debt mutual fund after understanding whether it fits their needs.

3. Hybrid Mutual Fund

A hybrid mutual fund combines equity and debt investments in one portfolio.

It tries to balance growth opportunities with comparatively lower volatility than a pure equity fund.

Suitable for:

- First-time investors

- Moderate risk takers

- Long-term investors seeking balance

Example

A newly married couple wants to begin investing but feels nervous about market ups and downs. A hybrid mutual fund may feel like a comfortable starting point because it mixes different types of investments.

4. Index Mutual Fund

An index mutual fund follows a market index instead of trying to beat it.

If the index goes up, the fund generally moves in a similar direction. If the index falls, the fund may also decline.

Suitable for:

- Beginners

- Long-term investors

- People looking for a simple investment approach

Example

Instead of choosing individual companies, an investor decides to invest in an index mutual fund that tracks a broad market index, allowing them to invest in many companies through one fund.

5. ELSS Mutual Fund

An ELSS (Equity Linked Savings Scheme) mutual fund is popular because it offers potential tax benefits under current Indian tax laws (subject to eligibility and applicable rules).

It also has a mandatory lock-in period.

Suitable for:

- Tax planning

- Long-term investors

- Salaried individuals

Example

A working professional wants to reduce taxable income while also investing for the future. After understanding the lock-in period and investment risks, they explore ELSS mutual funds as one possible option.

6. Liquid Mutual Fund

A liquid mutual fund is designed for short-term parking of money and generally invests in very short-duration debt instruments.

Many people use these funds when they may need access to their money in the near future, though they should still understand the fund’s features and risks.

Suitable for:

- Emergency savings

- Short-term goals

- Temporarily parking surplus money

Example

Someone receives a yearly bonus but hasn’t yet decided how to use it. Instead of leaving the entire amount idle for a short period, they explore whether a liquid mutual fund suits their needs.

A Thought from My Heart

One mistake I almost made was thinking there must be one “best mutual fund” for everyone. But after reading and talking with people who invest regularly, I realised that’s not how investing works.

The best mutual fund is the one that matches your goals, your budget, your investment period, and your comfort with risk—not simply the one someone else recommends.

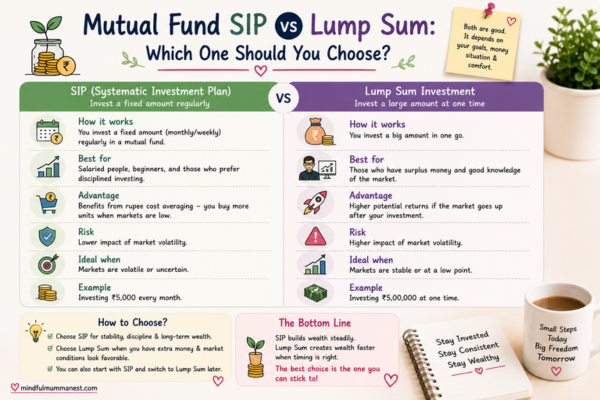

Mutual Fund SIP vs Lump Sum: Which One Should You Choose?

When I first started learning about mutual fund investing, one question kept coming up in every conversation—“Should I invest through SIP or should I invest a lump sum amount?” Honestly, I didn’t understand the difference at first. I thought investing was simply putting money into a mutual fund whenever possible.

After talking to friends and reading more, I realised both methods have their own purpose. Neither is universally better than the other. It depends on how you earn, how much money you have today, and what financial goals you’re working towards.

SIP and Lump Sum Are Two Different Ways to Invest in a Mutual Fund

Think of them as two different roads leading to the same destination.

The important thing isn’t choosing the “perfect” road—it’s choosing the one you can comfortably continue.

What is a SIP?

A Systematic Investment Plan (SIP) lets you invest a fixed amount in a mutual fund at regular intervals, usually every month.

Many beginners prefer SIP because it encourages disciplined investing without requiring a large amount of money at once.

Why many people like SIPs:

- Start with as little as ₹100 or ₹500 (depending on the scheme).

- Builds a regular saving habit.

- Easy to continue alongside monthly income.

- Reduces the temptation to wait for the “perfect” market time.

- Suitable for long-term financial planning.

Example

Let’s imagine Anjali earns ₹35,000 every month.

Instead of waiting until she saves ₹1 lakh, she starts investing ₹2,000 every month through a SIP.

Some months the market is high, some months it’s low, but she keeps investing regularly. Over time, this disciplined habit helps her stay invested without worrying about daily market movements.

What is a Lump Sum Investment?

A lump sum investment means investing a larger amount in one go instead of spreading it over regular intervals.

This approach is often considered by people who already have a significant amount available to invest.

A lump sum may suit people who:

- Receive a yearly bonus.

- Get maturity proceeds from an investment.

- Sell a property.

- Receive an inheritance.

- Already have idle savings they want to invest after careful planning.

Example

Rahul receives a ₹2 lakh annual bonus from his company.

After keeping money aside for emergencies and understanding his financial goals, he decides to invest part of the remaining amount as a lump sum in a mutual fund instead of leaving it unused in his bank account.

Mutual Fund SIP vs Lump Sum Comparison

| Feature | SIP | Lump Sum |

| Investment Style | Small regular investments | One-time investment |

| Starting Amount | Usually ₹100–₹500 onwards (scheme dependent) | Larger available amount |

| Best For | Salaried people, homemakers, students | Investors with surplus money |

| Investment Habit | Monthly discipline | One-time contribution |

| Market Timing | Less dependent on timing | Timing can have a bigger impact |

| Suitable For | Long-term investing | Investors with a clear plan and available funds |

Who Should Consider SIP?

From everything I’ve learned, SIP feels like one of the simplest ways for beginners to start a mutual fund journey.

It isn’t about investing a huge amount. It’s about creating consistency.

A SIP may suit:

- Homemakers.

- College students.

- Young professionals.

- Freelancers.

- Parents planning future goals.

- Anyone beginning their investment journey.

Who May Consider a Lump Sum?

A lump sum isn’t better—it simply fits different situations.

If someone already has money available and understands the risks involved, they may choose this method.

It may suit:

- Experienced investors.

- Business owners with surplus funds.

- People receiving bonuses.

- Retirees investing a planned amount.

- Investors with long-term goals and emergency savings already in place.

Example

Imagine two friends.

Sneha starts a ₹1,000 monthly SIP because that’s what comfortably fits her household budget.

Rohit receives ₹3 lakh after selling a piece of land and decides to invest part of it as a lump sum after understanding the risks and his financial plan.

Neither of them is making the “right” or “wrong” choice.

They’re simply choosing the investment method that suits their own financial situation.

A Thought from My Heart

One thing I learned while speaking to friends is that people often delay investing because they think they need a large amount first.

But many experienced investors told me something surprisingly simple:

“The habit of investing regularly is often more valuable than waiting for the perfect time or the perfect amount.”

That advice stayed with me because it reminded me that financial journeys are built step by step, not overnight.

Benefits of Mutual Fund Investing

When people hear the words mutual fund, they often think only about earning returns. I used to think the same. But the more I understood, the more I realised that the real benefit isn’t just about money growing—it’s also about building financial discipline, reducing the stress of choosing investments alone, and working towards long-term goals with patience.

Of course, every investment carries risk, and mutual funds are no exception. But when used thoughtfully, they can become an important part of a long-term financial plan.

Why So Many People Choose Mutual Funds

There isn’t one single reason why people invest in mutual funds.

Different people choose them for different stages of life, different dreams, and different financial goals.

1. You Can Start Small

One of the biggest surprises for me was learning that you don’t need lakhs of rupees to begin.

Many mutual fund schemes allow investments starting from ₹100 or ₹500 through SIPs.

Why this helps:

- Makes investing affordable.

- Encourages beginners.

- Suitable for homemakers and students.

- Removes the fear of needing a large amount.

Example

Instead of waiting until she saves ₹50,000, Meera starts with ₹500 every month. She focuses on consistency rather than the size of her first investment.

2. Professional Fund Management

Not everyone has time to study company reports or follow the stock market every day.

That’s where professional fund managers play an important role.

Benefits include:

- Market research.

- Portfolio management.

- Investment monitoring.

- Diversification decisions.

Example

A school teacher spends most of her day teaching and caring for her family. Rather than researching dozens of companies herself, she prefers a mutual fund where experienced professionals manage the investments.

3. Diversification

This was one concept that really made sense to me.

Instead of investing everything in one company, a mutual fund usually spreads investments across multiple assets.

Diversification may help:

- Reduce concentration risk.

- Balance different sectors.

- Avoid depending on a single company.

- Create a broader investment portfolio.

Example

Imagine investing all your savings in just one company. If that company performs poorly, your investment may be heavily affected.

A diversified mutual fund, on the other hand, may invest across banking, IT, healthcare, manufacturing, energy, and other sectors instead of relying on only one business.

4. Builds Financial Discipline

This is probably my favourite benefit.

A monthly SIP quietly teaches you something beyond investing—it teaches consistency.

It helps you:

- Save regularly.

- Invest before unnecessary spending.

- Build long-term habits.

- Stay committed to your financial goals.

Example

A young couple decides that every month, before shopping or eating out, they will first invest ₹2,000 through their SIP. Over time, investing becomes part of their routine instead of an occasional decision.

5. Supports Long-Term Wealth Creation

Mutual funds are generally considered more suitable for long-term goals rather than short-term speculation.

Time allows investments to experience market cycles and gives compounding more opportunity to work.

Long-term goals may include:

- Child’s education.

- Retirement planning.

- Buying a home.

- Building future wealth.

- Financial independence.

Example

Parents start investing shortly after their daughter is born with the goal of supporting her higher education many years later. They review their investments periodically while staying focused on the long-term objective.

A Thought from My Heart

The biggest lesson I learned wasn’t that mutual funds make people rich.

It was that they help ordinary people become more disciplined with money.

Sometimes the greatest return isn’t just what appears in your investment statement—it’s the confidence that comes from knowing you’re taking small, consistent steps towards a better financial future.

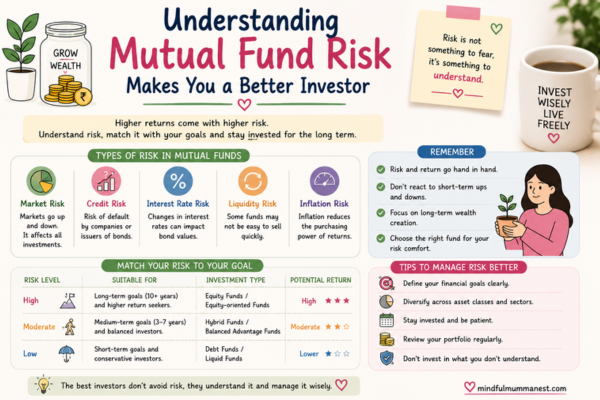

Risks of Mutual Fund Investing You Should Never Ignore

When I first started understanding mutual fund investing, I came across many people who only talked about returns. Very few spoke about the risks. That made me realise something important—if we only look at the good side of investing, we aren’t making informed decisions.

A mutual fund can help you work towards your financial goals, but it is not a guaranteed income plan. Like every market-linked investment, it comes with risks. Knowing these risks doesn’t mean we should be afraid. It simply helps us become wiser and more patient investors.

Understanding Mutual Fund Risk Makes You a Better Investor

One friend told me something that has stayed with me:

“Don’t invest because someone says it’s the best. Invest because you understand what you’re investing in.”

That simple advice changed the way I looked at mutual funds.

1. Market Risk

The biggest risk in a mutual fund is market risk.

When the stock market rises, the value of your investment may increase. When the market falls, your mutual fund value may also decline. This is completely normal and happens to every market-linked investment.

Remember:

- Markets move up and down.

- Short-term losses are possible.

- Long-term investing often helps ride out market fluctuations, but it does not eliminate risk.

- Avoid making decisions based only on temporary market movements.

Example

Imagine you invest ₹2,000 every month through SIP.

After six months, the market suddenly falls.

Instead of panicking and stopping your investment, you understand that market ups and downs are a natural part of investing and continue according to your long-term plan.

2. Choosing the Wrong Mutual Fund

Not every mutual fund is suitable for every person.

Many beginners simply invest because someone else recommended a scheme without understanding whether it matches their own goals.

Before investing, ask yourself:

- Why am I investing?

- How long can I stay invested?

- How much risk am I comfortable taking?

- Do I need this money soon?

Example

A person saving for next year’s family vacation invests in a high-risk equity mutual fund without understanding its purpose. Since the goal is only one year away, the fund may not match their needs if the market becomes volatile.

3. Expecting Quick Profits

This is probably one of the most common mistakes.

Some people think mutual funds will double their money within months.

That’s simply not how long-term investing works.

Keep realistic expectations:

- Wealth usually takes time to build.

- Markets don’t move upward every month.

- Patience is an important part of investing.

- Consistency matters more than chasing quick returns.

Example

Two friends start investing together.

One keeps checking the app every day and becomes anxious with every market movement.

The other reviews the investment occasionally and stays focused on a long-term goal.

After several years, the second friend is often less stressed because they invested with realistic expectations.

4. Inflation Risk

Sometimes people keep all their savings in places where the money grows very slowly.

While safety is important, inflation can gradually reduce the purchasing power of money over time.

This is one reason people explore different investment options as part of a balanced financial plan.

Think about it:

- Prices generally rise over time.

- Education becomes more expensive.

- Healthcare costs increase.

- Everyday living expenses also grow.

Example

If a family plans for a child’s college education 15 years from now, they need to consider that the future cost may be much higher than today’s cost due to inflation.

5. Emotional Investing

This risk surprised me the most because it has nothing to do with the market.

It has everything to do with us.

Fear, excitement, rumours, and social media can influence investment decisions if we’re not careful.

Avoid investing because:

- Everyone else is doing it.

- Someone promises guaranteed high returns.

- A social media post says it’s the “best” investment.

- Friends pressure you without understanding your goals.

Example

Rohan hears everyone talking about one particular mutual fund.

Without reading anything about it, he invests immediately.

Later he realises the fund doesn’t match his investment period or comfort with risk.

A little patience and research could have helped him make a more informed decision.

A Thought from My Heart

One thing I learned from my conversations with friends is that successful investing isn’t about avoiding every market fall.

It’s about understanding that ups and downs are part of the journey.

The more we learn before investing, the less likely we are to panic when markets fluctuate.

Who Should Invest in a Mutual Fund?

When I first heard about mutual fund investing, I honestly thought it was only for people working in big companies or earning high salaries.

But after learning more, I realised that’s one of the biggest misconceptions.

A mutual fund isn’t designed for one type of person.

It’s simply an investment option that different people may choose depending on their financial goals, investment period, and comfort with market risk.

A Mutual Fund Can Be Useful at Different Stages of Life

Our goals change as life changes.

The right investment isn’t based on your age alone—it’s based on what you’re planning for.

1. Homemakers

Managing a home also means managing money wisely.

Even small monthly savings can become meaningful when invested thoughtfully over the long term.

Why it may help:

- Builds financial confidence.

- Encourages disciplined saving.

- Supports future family goals.

- Can begin with a small SIP, depending on the scheme.

Example

A homemaker saves ₹500 every month from her household budget.

Instead of keeping the money unused, she explores starting a SIP after learning about mutual funds and understanding whether it suits her financial goals.

2. Students

One lesson I wish more young people learned is that investing is not only about money—it’s also about developing good habits early.

Starting small can teach discipline and long-term thinking.

Students can learn to:

- Save regularly.

- Understand personal finance.

- Think about long-term goals.

- Develop responsible money habits.

Example

A college student saves ₹300 each month from pocket money and begins learning about investing without feeling the pressure to invest large amounts.

3. Salaried Professionals

For many working people, a monthly salary makes SIP investing convenient.

A fixed date and fixed amount can help make investing part of the monthly routine.

Helpful for:

- Retirement planning.

- Buying a house.

- Children’s education.

- Long-term wealth creation.

Example

After receiving his salary every month, Amit invests ₹3,000 through SIP before spending on non-essential purchases.

4. Parents

Every parent dreams about giving their children a secure future.

Long-term investing can become one way of working towards those dreams.

Common goals include:

- Higher education.

- Marriage planning.

- Family financial security.

- Long-term wealth creation.

Example

Parents begin investing shortly after their child is born with the hope of building a fund that may support future education expenses.

5. Freelancers and Business Owners

Income may not always be fixed, but planning for the future is still important.

Many freelancers choose to invest whenever cash flow allows while keeping emergency savings separate.

It may help with:

- Long-term planning.

- Building financial discipline.

- Creating future wealth.

- Managing irregular income more thoughtfully.

Example

A graphic designer receives payments from different clients every month.

Whenever extra income is available after essential expenses and emergency savings, a portion is invested according to a long-term plan.

6. Retired Individuals

Even after retirement, financial planning doesn’t stop.

Some retirees explore mutual funds based on their income needs, investment horizon, and risk tolerance, often after seeking appropriate financial guidance.

Important considerations:

- Regular income needs.

- Capital preservation.

- Healthcare planning.

- Suitable investment choices.

Example

A retired couple reviews different investment options with the aim of balancing safety and growth according to their financial situation.

A Thought from My Heart

The biggest thing I understood is this:

There isn’t a “perfect age” to start investing.

There is only a “better time”—and that’s when you understand what you’re doing, have your emergency savings in place, and can invest an amount you’re comfortable leaving invested for your chosen goal.

The amount matters less than the habit. The habit, repeated patiently over the years, is what often makes the real difference.

Can You Start a Mutual Fund with ₹100 or ₹500?

This was probably the biggest question on my mind when I first started learning about mutual fund investing.

I used to believe investing was only for people who had lakhs of rupees sitting in their bank accounts. Every time someone mentioned investments, I quietly thought, “Maybe one day, when I have enough money.” But after speaking with friends and reading trusted resources, I realised I had been looking at it the wrong way.

The truth is, many mutual fund schemes in India allow you to start with a small SIP—sometimes as low as ₹100 or ₹500, depending on the scheme. It isn’t about how much you begin with. It’s about building the habit of investing consistently while keeping realistic expectations.

Small Amounts Can Build Big Habits

One thing almost every experienced investor told me was this:

“Don’t underestimate a small beginning.”

That sentence stayed with me because it applies to almost everything in life—not just investing.

Why Starting Small Can Still Be Meaningful

Many people delay investing because they think their savings are “too small.”

But small savings can become the foundation of a long-term financial habit.

Starting small may help you:

- Develop the habit of investing regularly.

- Learn how mutual funds work without committing a large amount.

- Build confidence as you gain experience.

- Increase your investment gradually as your income grows.

- Stay financially disciplined.

Example 1 – A Homemaker

Let’s imagine Neha.

She manages her household expenses carefully.

Some months she saves:

- ₹20 from the vegetable budget.

- ₹30 from grocery shopping.

- ₹50 from milk expenses.

- ₹100 from avoiding unnecessary online shopping.

- ₹300 from careful monthly budgeting.

By the end of the month, she has managed to save around ₹500.

Earlier, she would simply leave this money in a drawer.

Now, after understanding SIPs, she decides to invest ₹500 every month in a mutual fund that matches her goals.

She isn’t expecting miracles.

She’s building a financial habit.

One month becomes another.

Then another year.

That’s how consistency begins.

Example 2 – A College Student

Rahul receives ₹3,000 as monthly pocket money.

Instead of spending everything on food delivery or impulse purchases, he decides to save ₹300 every month.

He starts learning about mutual funds while investing a small amount through SIP.

The money may be small today, but the lesson he learns about financial discipline may stay with him for life.

Example 3 – A Young Professional

Pooja gets her first salary.

She wants to enjoy it, buy gifts for her parents, and also plan for the future.

Instead of waiting until she earns much more, she begins with a ₹1,000 monthly SIP.

As her salary increases over the years, she gradually increases her SIP too.

She doesn’t try to become rich overnight.

She simply grows her investment habit along with her income.

The Power of Consistency

When I spoke to friends who had been investing for several years, one thing was common among almost all of them.

None of them said,

“I became successful because I invested one huge amount.”

Instead, they kept repeating something much simpler.

They said,

“I kept investing, even when the amount was small.”

That made me realise that investing isn’t only about money.

It’s also about patience, discipline, and staying committed to your future goals.

Can Small SIPs Really Make a Difference?

Yes—but it’s important to understand how.

A small SIP is unlikely to make someone wealthy in a short time. What it can do is help you build the habit of investing and give your money time to benefit from compounding if your investments grow over the long term. Consistency and time often matter more than trying to start with a very large amount.

That’s why many beginners prefer SIPs because they:

- Fit comfortably into monthly budgets.

- Encourage regular investing.

- Reduce the pressure of investing a large amount at once.

- Help create long-term financial discipline.

- Can be increased gradually as income grows.

A Thought from My Heart

One of my friends told me something so simple that I wrote it down.

“Your first investment doesn’t have to change your life. It only has to change your habit.”

I think that’s one of the most beautiful lessons I learned.

Whether you begin with ₹100, ₹500, or ₹1,000, what truly matters is that you’re taking a thoughtful step towards your future instead of waiting for the “perfect” time.

10 Mindful Rules Before You Invest in a Mutual Fund

Before writing this blog, I kept asking myself one question.

“If someone from my own family wanted to start investing today, what advice would I honestly give them?”

These are the lessons that came up again and again during my conversations with friends and while reading trusted financial resources.

These aren’t complicated investment strategies.

They’re simple habits that can help you become a more mindful investor.

Good Investing Begins with Good Habits

A mutual fund is just one investment option.

The real strength comes from how thoughtfully you approach investing.

1. Build an Emergency Fund First

Before investing, try to keep some money aside for unexpected situations like medical emergencies, job loss, or urgent household expenses.

Investing becomes much less stressful when you know you have a financial cushion.

2. Never Invest Borrowed Money

Loans and investments should not be mixed casually.

Borrowed money adds pressure, and market-linked investments can fluctuate.

Invest only the money you can comfortably leave invested for your chosen goal.

3. Understand the Mutual Fund Before Investing

Don’t invest just because someone says,

“This fund is giving great returns.”

Take a little time to understand:

- What the fund invests in.

- Its investment objective.

- The level of risk involved.

- Whether it matches your goals.

4. Don’t Expect Guaranteed Returns

This was one of the biggest lessons I learned.

Mutual funds are linked to the market.

Some years may be good.

Some years may not.

Patience is an important part of investing.

5. Invest for Your Goals, Not Someone Else’s

Your friend’s investment plan doesn’t have to become yours.

Everyone has different:

- Income.

- Responsibilities.

- Dreams.

- Financial goals.

- Comfort with risk.

Choose investments that suit your own journey.

6. Review, Don’t Panic

Checking your investment every hour won’t help it grow.

Instead:

- Review it periodically.

- Stay informed.

- Avoid emotional decisions during market ups and downs.

7. Increase Your SIP Whenever Possible

As your salary or income grows, consider increasing your SIP if it fits your budget and financial plan.

Even a small increase each year can make a meaningful difference over the long term.

8. Diversify Your Investments

Don’t depend entirely on one investment option.

Many people build a balanced financial plan that includes emergency savings and other suitable investments alongside mutual funds.

9. Keep Learning

The financial world keeps changing.

Continue learning through trusted resources.

The more you understand, the more confident your decisions become.

10. Invest with Patience

Perhaps this is the most important lesson of all.

We live in a world that wants instant results.

Investing usually rewards patience much more than hurry.

A Thought from My Heart

If there’s one thing this journey has taught me, it’s that successful investing isn’t about predicting the market.

It’s about creating good habits, staying patient, and making decisions you truly understand.

That’s the kind of financial confidence I hope every reader of Mindful Mumma Nest builds—not by chasing shortcuts, but by learning one thoughtful step at a time.

Common Mutual Fund Mistakes Beginners Should Avoid

I’ll be honest. While learning about mutual fund investing, I realised that most people don’t lose confidence because they chose the wrong app or the wrong SIP date. They lose confidence because they begin with unrealistic expectations or follow advice without understanding it.

Almost every experienced investor I spoke to had one thing in common—they all admitted they had made mistakes in the beginning. The difference was that they learned from those mistakes instead of giving up.

If you’re just starting your mutual fund journey, avoiding these common mistakes can save you a lot of unnecessary stress.

A Few Smart Decisions Today Can Prevent Bigger Mistakes Tomorrow

Nobody becomes a perfect investor overnight.

Learning is part of the journey, and making informed decisions is far better than making rushed ones.

1. Investing Without Understanding the Mutual Fund

Sometimes we hear a colleague, neighbour, or relative say,

“This mutual fund gave amazing returns. You should invest too.”

It sounds tempting.

But what suits one person may not suit another.

Before investing, always understand:

- What the fund invests in.

- Its investment objective.

- Whether it matches your financial goals.

- The level of risk involved.

- How long you plan to stay invested.

Example

Riya invested in a mutual fund simply because her office friends recommended it.

A year later, she realised the fund didn’t match her short-term goal of buying a car.

A little research beforehand could have helped her choose a more suitable option.

2. Expecting Quick Money

This is probably the biggest misunderstanding about mutual funds.

Some people expect their investment to double within months.

That’s not how long-term investing usually works.

Remember:

- Markets go up and down.

- Mutual funds are not a shortcut to becoming rich.

- Wealth generally grows through patience and consistency.

- Long-term goals often benefit from staying invested through market cycles.

Example

Rohan invested for only six months and became disappointed when markets declined.

His friend, who continued investing patiently over several years according to her plan, experienced both market highs and lows while staying focused on long-term goals.

3. Stopping SIP During Market Falls

When markets fall, many beginners panic.

Ironically, that’s when some people stop investing.

One friend explained it beautifully:

“When your favourite clothes go on sale, you feel happy. But when markets fall, people become afraid. Why?”

That question really made me think.

Instead of panicking:

- Understand why markets are falling.

- Review your financial goals.

- Avoid emotional decisions.

- Stay disciplined if your long-term plan hasn’t changed.

Example

Sneha continued her ₹2,000 SIP even during a market correction because her goal was still many years away.

She focused on her long-term plan instead of reacting to short-term headlines.

4. Investing Without Financial Goals

Money needs a purpose.

Otherwise, it’s easy to lose motivation.

Before starting a mutual fund, ask yourself:

“Why am I investing?”

Your goal might be:

- Child’s education.

- Buying a house.

- Retirement.

- Emergency planning.

- Financial independence.

- Building long-term wealth.

Example

Two friends invested the same amount.

One invested randomly.

The other invested with a clear goal of funding her daughter’s higher education.

Having a clear purpose helped her stay committed over the years.

5. Ignoring Emergency Savings

This lesson came up in almost every conversation I had.

Never invest money you might urgently need next month.

- Unexpected situations happen.

- Medical expenses.

- Job changes.

- Family emergencies.

That’s why an emergency fund is so important.

Example

If someone invests all their savings and suddenly needs money for a medical emergency, they may have to withdraw their investment at an inconvenient time.

Keeping emergency savings separate can provide greater financial flexibility.

6. Following Social Media Blindly

Today we see investment tips everywhere.

- Instagram.

- YouTube.

- WhatsApp.

Telegram.

Some advice is helpful.

Some isn’t.

Always verify information before making financial decisions.

Ask yourself:

- Is the source trustworthy?

- Does this advice suit my financial goals?

- Have I understood the risks?

- Am I investing because I understand it—or because everyone else is talking about it?

Example

Arjun saw a viral video calling one mutual fund the “best investment.”

Instead of investing immediately, he spent a few days learning about the fund and realised it didn’t match his own financial needs.

That small pause helped him make a better-informed decision.

A Thought from My Heart

The biggest mistake isn’t choosing the wrong mutual fund.

The biggest mistake is investing without learning.

The more I read, asked questions, and spoke with experienced friends, the more confident I became.

And honestly, I think that’s a lesson that applies to every area of life—not just investing.

Mutual Fund vs Stock Market: What’s the Difference?

When I published my blog on Stock Market and Share Market, many readers asked me another important question.

“If mutual funds also invest in shares, then what’s the difference between buying shares directly and investing in a mutual fund?”

I had the same doubt in the beginning.

After understanding both, I realised they serve different purposes.

Neither is better than the other.

It depends on how involved you want to be in managing your investments.

Mutual Fund and Stocks Are Related—but Not the Same

Think of it this way.

Buying individual shares is like cooking every meal yourself.

Investing in a mutual fund is like asking an experienced chef to prepare a balanced meal using carefully selected ingredients.

Both have value.

The choice depends on your knowledge, time, and comfort.

| Feature | Mutual Fund | Stock Market (Direct Shares) |

| Who manages the investment? | Professional fund manager | You make every decision |

| Number of investments | Usually many companies and assets | You choose individual companies |

| Diversification | Generally diversified | Depends on what you buy |

| Research required | Comparatively less | Much more |

| Suitable for | Beginners and long-term investors | People willing to research companies |

| Time commitment | Lower | Higher |

| Market risk | Present | Present, often more concentrated in individual holdings |

| Starting point | Many schemes allow small SIPs | Depends on the share price and your strategy |

Example

Imagine you have ₹5,000.

Option 1: You buy shares of one or two companies after doing your own research.

Option 2: You invest ₹5,000 in a mutual fund that may already hold investments across dozens of companies and other assets, depending on the scheme.

Both options involve market risk.

The difference is that in a mutual fund, professional managers make the investment decisions, while in direct stock investing, those decisions are entirely yours.

A Thought from My Heart

After learning about both, I realised something important.

You don’t have to choose one because someone else says it’s better.

Choose the option that matches your knowledge, your confidence, your financial goals, and the amount of time you can dedicate to understanding your investments.

For many beginners, learning through mutual funds can feel like a more comfortable first step before deciding whether direct stock investing is right for them.

Mutual Fund Tax in India: What Every Beginner Should Know

When I first started learning about mutual fund investing, I focused only on one thing—returns. Later, during a conversation with a friend, they asked me,

“Have you also understood how mutual fund tax works?”

Honestly, I hadn’t.

That’s when I realised investing isn’t just about choosing a mutual fund. It’s also about understanding what happens when you earn gains or withdraw your investment.

Don’t worry—this section isn’t meant to confuse you with complicated tax laws. My aim is simply to help you understand the basics so you know what to look for before investing.

Understanding Mutual Fund Tax Is Part of Smart Investing

Taxes may sound boring, but learning the basics can help you make better financial decisions.

The good news is that once you understand the difference between the types of mutual funds and the time you stay invested, everything becomes much easier.

Things Every Beginner Should Know

- Mutual funds and taxes are connected.

- Tax rules can differ depending on the type of mutual fund.

- How long you stay invested may also affect taxation.

- Tax laws can change over time, so always check the latest rules before making financial decisions.

- If you’re unsure, consider consulting a qualified tax professional or financial advisor.

Example

Imagine two friends invest in different mutual funds.

One keeps the investment for several years.

The other withdraws the money much earlier.

Even if both invested the same amount, the tax treatment may not be exactly the same because it depends on the applicable rules, the type of fund, and the holding period.

That’s why understanding tax basics is just as important as understanding returns.

What About ELSS Mutual Funds?

While learning about different mutual funds, I found that many people also talk about ELSS (Equity Linked Savings Scheme).

The reason is simple.

Besides being a mutual fund, ELSS has traditionally been used by eligible investors as a tax-saving investment under applicable Indian tax provisions.

However, tax benefits depend on the tax regime you choose and the rules in force at that time.

ELSS at a Glance

- It is a type of equity mutual fund.

- It has a mandatory lock-in period.

- It is often considered by people planning their taxes.

- It also carries market risk because it invests mainly in equities.

Example

A salaried employee plans investments at the beginning of the financial year.

While exploring different options, they also compare ELSS with other tax-saving choices before deciding what best suits their financial plan.

A Thought from My Heart

One thing I’ve learned is that understanding tax isn’t only about saving money.

It’s about becoming a more informed investor.

Even if the topic feels a little technical today, spending a few minutes learning it can help you avoid confusion later.

Best Mutual Fund Apps for Beginners in India

After understanding what a mutual fund is, the next question naturally came to my mind:

“Where do people actually invest?”

- Friends suggested different apps.

- Some liked one because it was simple.

- Others preferred another because they already used it for stocks.

- I realised that there isn’t one “perfect” app for everyone.

- The best app is the one you understand, trust, and feel comfortable using.

Before choosing any platform, always ensure it is registered with the appropriate regulatory authorities where applicable and offers the features you need.

Choose an App That Makes Investing Easy to Understand

A good investment app shouldn’t just help you invest.

It should also help you learn.

As a beginner, I would always choose simplicity over unnecessary features.

1. Groww

One of the most popular choices among beginners.

Many people appreciate its clean interface and simple investment process.

Why people like it:

- Beginner-friendly.

- Easy account setup.

- Mutual funds, stocks, and other investment options in one place.

- Educational content for new investors.

Example

A first-time investor who has never used an investment app may find Groww’s simple layout easier to understand while learning the basics.

2. Zerodha Coin

If you’re already familiar with the Zerodha ecosystem, Coin is another popular option for investing in mutual funds.

Features include:

- Direct mutual funds.

- Easy portfolio tracking.

- Integration with Zerodha accounts.

- Simple investment management.

Example

Someone already investing in shares through Zerodha may prefer using Coin to manage mutual funds in the same ecosystem.

3. ET Money

Many beginners know ET Money not only for investing but also for personal finance tools.

It combines investing with features related to financial planning.

Useful for:

- Mutual fund investing.

- Goal planning.

- Expense tracking.

- Financial insights.

Example

A young professional who wants to manage both monthly expenses and investments from one platform may find ET Money useful.

4. Upstox

Originally popular for stock investing, Upstox also offers mutual fund investment options.

Many investors like having multiple investment choices available in one app.

Highlights include:

- Mutual funds.

- Stocks.

- Portfolio management.

- Mobile investing.

Example

Someone interested in learning both mutual funds and direct stock investing may prefer a platform that supports both.

5. Angel One

Angel One is another well-known investment platform used by many Indian investors.

Along with mutual funds, it also provides access to several other investment products.

Features include:

- Mutual fund investing.

- Stock market access.

- Research tools.

- Investment tracking.

Example

An investor planning to gradually expand their financial knowledge may appreciate having different investment options within one platform.

What Should You Look for Before Choosing a Mutual Fund App?

Instead of selecting an app only because it is popular, I think it’s better to ask yourself a few simple questions.

Look for:

- Easy-to-understand interface.

- Secure login and account protection.

- Transparent information.

- Goal-based investing features.

- Good customer support.

- Educational resources for beginners.

- Simple portfolio tracking.

- Regular app updates.

A Thought from My Heart

One thing I realised during my learning journey is that an app doesn’t make someone a successful investor.

Our habits do.

An app is only a tool.

What truly matters is learning patiently, investing thoughtfully, and staying consistent with your financial goals.

Guest Corner with Gratitude

Before I end this guide, I want to express my heartfelt gratitude to everyone who has helped make financial education easier for ordinary people like us.

When I first started learning about mutual funds, I didn’t rely on just one source. I listened to friends who had practical investing experience, read educational articles, explored beginner-friendly platforms, and referred to trusted organisations that work to spread financial awareness.

A sincere thank you to AMFI (Association of Mutual Funds in India) for promoting investor education, SEBI (Securities and Exchange Board of India) for protecting investors and strengthening India’s financial markets, NSE and BSE for making market information accessible, and educational platforms such as Groww, Zerodha, ET Money, Upstox, Angel One, Value Research, and Morningstar for helping beginners understand investing in a simpler way.

And finally, thank you to my friends who patiently answered my endless questions, shared their experiences, and reminded me that every confident investor was once a beginner too.

Sometimes, the greatest learning doesn’t come from complicated books—it comes from honest conversations with people who are willing to share what they have learned.

Final Thoughts

When I started learning about mutual funds, I realised they aren’t only for finance experts or wealthy people. They’re for anyone willing to learn, stay patient, and plan for the future.

I’m not a market analyst. I’m simply sharing what I understood through conversations with friends, trusted resources, and my own learning journey. If this guide has helped you understand mutual funds a little better, then it has served its purpose.

Start small, keep learning, invest wisely, and remember—consistency often matters more than the amount you begin with.

Frequently Asked Questions (FAQs)

1. What is a mutual fund?

A mutual fund pools money from many investors and is managed by professionals.

2. Can I start investing with ₹100 or ₹500?

Yes, many mutual fund SIPs allow small investments depending on the scheme.

3. Is a mutual fund safe?

Mutual funds are market-linked investments, so returns are not guaranteed.

4. What is SIP?

SIP is a way to invest a fixed amount regularly in a mutual fund.

5. Can homemakers invest in mutual funds?

Yes, anyone with financial goals and regular savings can invest.

6. Should I choose SIP or Lump Sum?

Choose SIP for regular investing and Lump Sum if you already have surplus money.

7. Can I lose money in a mutual fund?

Yes, mutual fund values can rise or fall with market performance.

8. What should I check before investing?

Understand your goals, the fund’s objective, risks, and investment horizon.

Sources & Tools

- AMFI – Investor education and mutual fund awareness.

- SEBI – India’s securities market regulator.

- NSE India – Market information and financial learning.

- Value Research – Mutual fund research and comparisons.

- Groww Learn – Beginner-friendly investment guides.

- Google Keyword Planner & Google Trends – Keyword research and search trends for SEO.

Disclaimer

This blog is shared for educational purposes based on my personal learning and trusted resources. Mutual funds are subject to market risks. Please read all scheme-related documents carefully before investing.